The diploma is on the wall, the cap is in the back of the closet, and you’ve finally landed that first real job. It’s a great feeling until the first of the month rolls around. Now, you're not just managing a course load; you’re managing a life. For most of us, financial literacy for graduates is the one "required course" we never actually got a syllabus for.

Your degree got you through the door, but knowing what to do with your paycheck is what gives you long-term freedom. Let’s look at how to handle your money without the soul-crushing stress.

The First Paycheck: Why Is It So Small?

There is a specific, painful kind of sticker shock that happens when you open your first professional paystub. You signed an offer for $5,000 a month, but only $3,700 actually hit your bank account. Where did the rest go? Understanding the gap between gross income (the big number on your contract) and net pay (what you can actually spend) is the first step to staying afloat.

When you look at that stub, you’re seeing the "adulting" tax in real-time:

- Federal and State Income Tax: Based on that confusing W-4 you signed on your first day.

- FICA: Your mandatory contribution to Social Security and Medicare.

- Health Insurance: Your slice of the premium for medical, dental, and vision.

- Retirement: The money you’re (hopefully) sending to your 401(k).

The easiest way to manage this? Set up your direct deposit to split automatically. If $200 goes straight to savings and the rest goes to checking, you won’t even miss it. It’s the classic "pay yourself first" move.

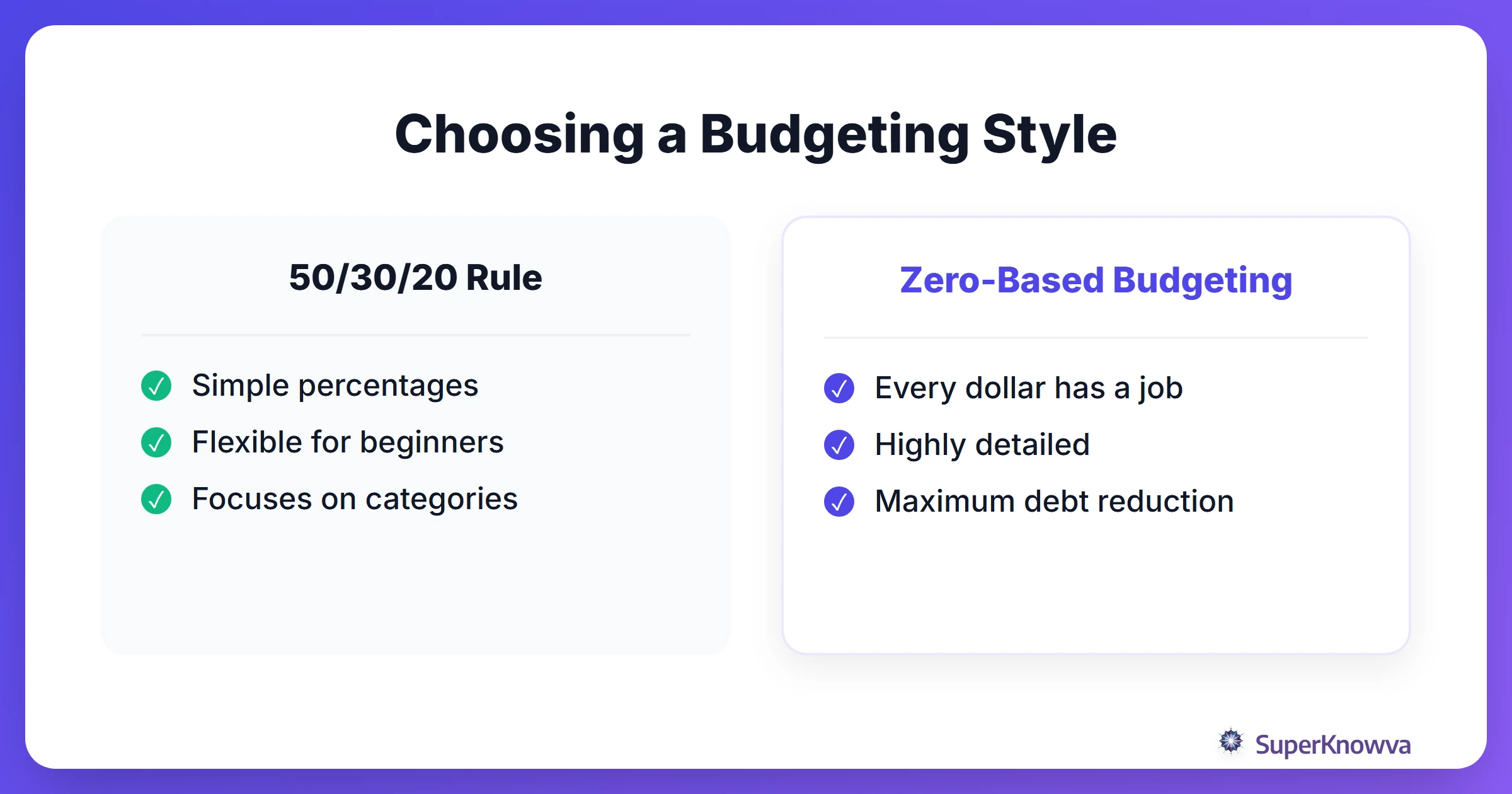

Creating a Budget That Doesn't Suck

Transitioning from the dining hall to the real world is expensive. Between security deposits and professional clothes, navigating the transition to the workplace is a financial gauntlet. Budgeting for new professionals isn't about living on ramen noodles; it’s about making sure your money goes where you actually want it to go.

Try the 50/30/20 rule:

- 50% for Needs: Rent, groceries, and utilities.

- 30% for Wants: Happy hours, weekend trips, and an updated wardrobe.

- 20% for Savings and Debt: This covers student loans and emergencies.

Don't forget the hidden costs. Renters' insurance and professional dues have a way of sneaking up on you. Apps like YNAB or Rocket Money can help, but the "why" is more important than the tool. Even state education boards, like those following the JumpStart National Standards for Personal Finance, emphasize that intentionality is the secret sauce to building wealth.

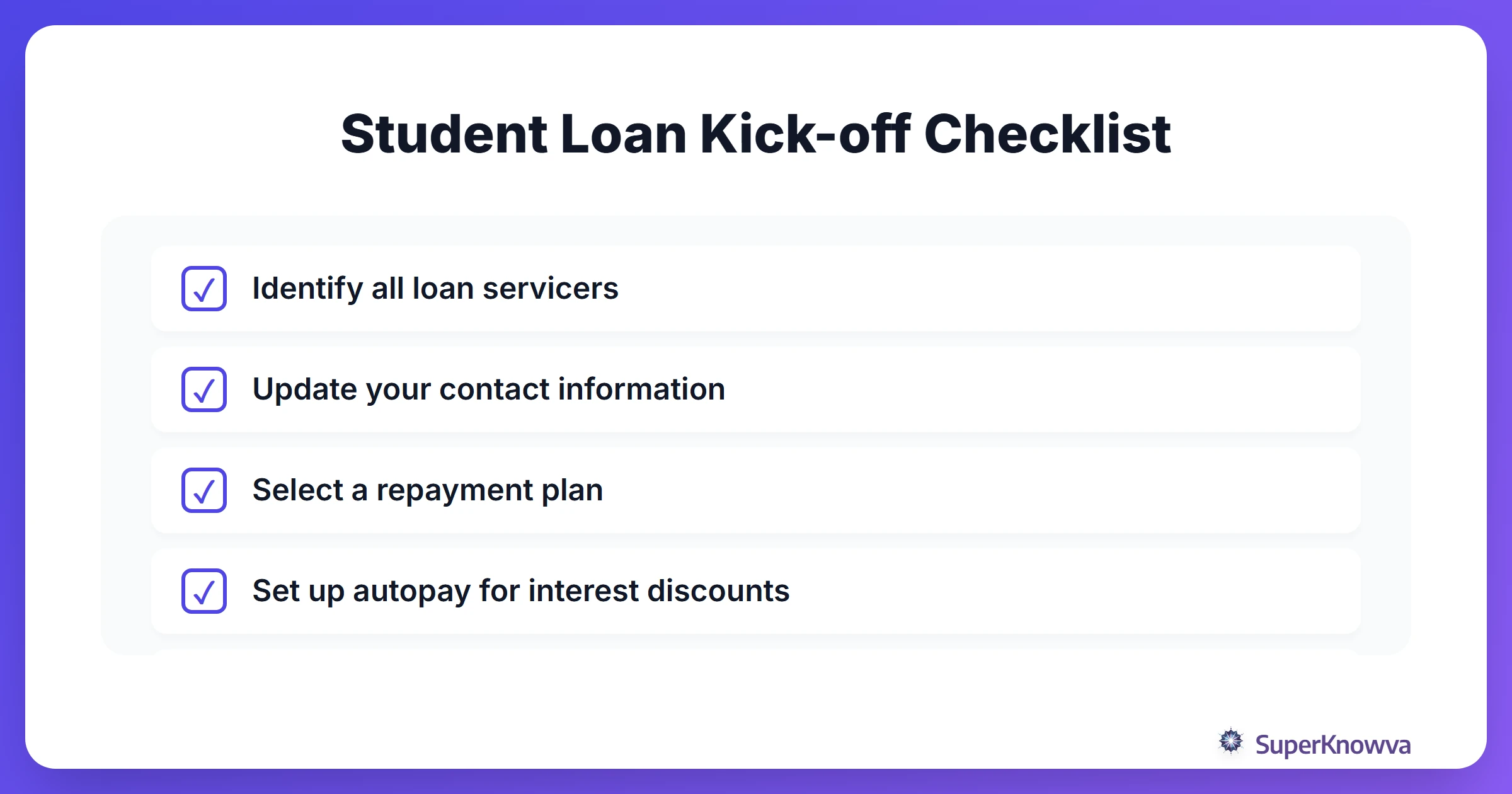

Facing the Student Loan Giant

For most of us, debt feels like a dark cloud. But ignoring it only makes it rain harder. Effective student loan repayment strategies start with a simple inventory: who do you owe, and at what interest rate? Most federal loans give you a six-month grace period, but remember: interest is often still ticking in the background.

You have options. If you’re in a high-paying role, the Standard Repayment plan gets you debt-free in 10 years. If things are tight, an Income-Driven Repayment (IDR) plan adjusts your bill based on what you actually earn.

Want to kill the debt faster? Use the Avalanche method (hit the highest interest rate first) to save the most money, or the Snowball method (pay off the smallest balance first) if you need a quick psychological win to stay motivated.

Building Your "Life Happens" Fund

Before you start picking individual stocks, you need a safety net. Emergency fund basics suggest saving 3 to 6 months of living expenses. Why? Because cars break, roommates move out, and sometimes jobs disappear. Having that cash sitting in the bank allows you to focus on building professional connections without the constant "what if" anxiety.

Put this money in a High-Yield Savings Account (HYSA). It’s still your money, but it earns way more interest than a standard checking account. Just remember: a "financial emergency" is an unexpected root canal, not a 40% off sale at your favorite store.

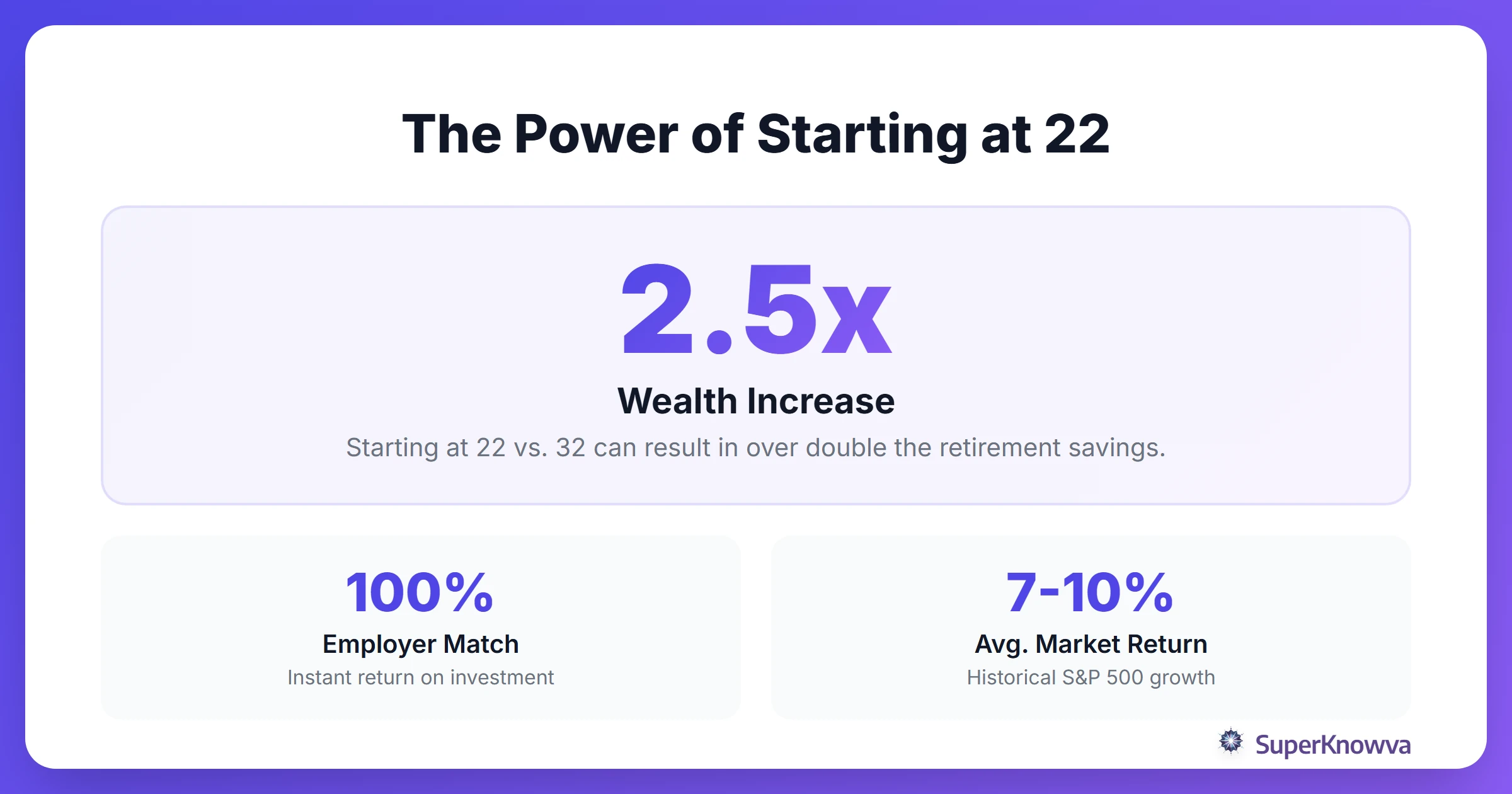

Investing: Why 22 is Better Than 32

When it comes to investing for beginners, time is your greatest superpower. Thanks to compound interest, a single dollar invested in your early 20s is worth far more than a dollar invested a decade later. It’s the closest thing to "free money" you’ll ever find.

If your company offers a 401k for new hires with a "match," take it. Seriously. It’s a 100% return on your investment before the market even moves. Once you’ve got that, look into IRAs:

- Roth IRA: You pay taxes now, but your future self gets every penny tax-free.

- Traditional IRA: You get a tax break today, but you’ll pay the IRS when you retire.

And don't forget: Personal Branding for Students and new grads is an investment, too. Your ability to earn is your biggest asset, so keep sharpening your skills.

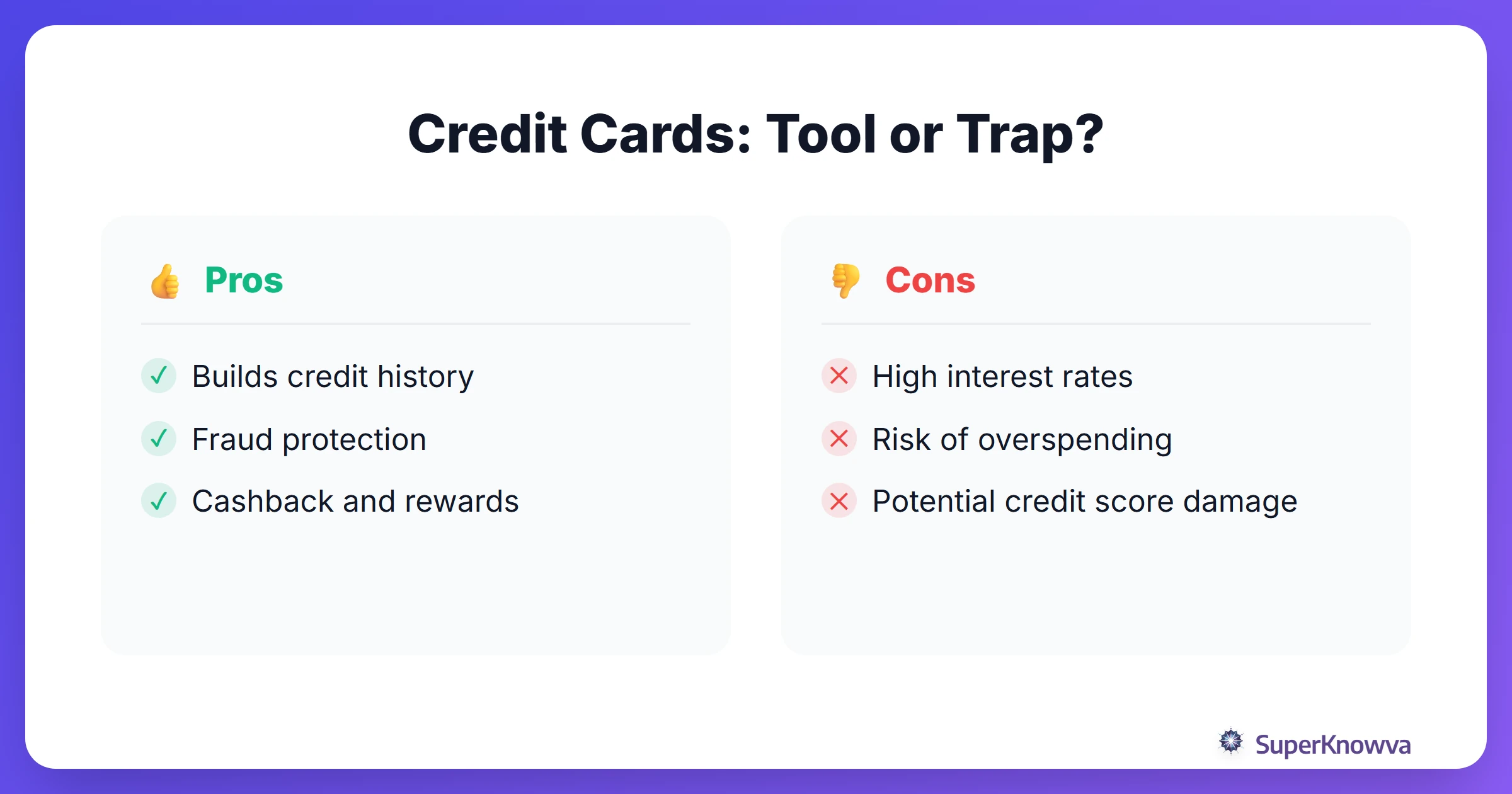

Your Credit Score is Your Financial Resume

Think of your credit score as a grade for how well you handle money. It determines if you can rent that dream apartment or get a decent rate on a car loan. It’s so vital that states like Rhode Island have integrated it into their Rhode Island Financial Literacy Standards.

Keep your score high with three simple rules:

- Never be late: Set up autopay for the minimum at the very least.

- Watch the limit: Try not to use more than 30% of your available credit.

- Check the stats: Use a free tool to monitor your report for errors.

Managing your money early isn't about becoming rich overnight. It's about creating a plan so that in five years you aren't just surviving; you're thriving. Start small, stay consistent, and reach your financial goals.